Oversupply is one of the biggest risks in property investing 🏡 In this episode, we break down how to spot areas at risk of too much stock and what to look for before buying. We’ll show you why counting listings isn’t enough, how to use Google Maps to predict future...

You don’t make money when you buy

You don’t make money when you buy

INTRODUCTION

How many times have you heard someone say, “You make money when you buy?”

I’ve bought 16 investment properties and never made a single cent … when I bought. The only time I’ve ever made money is when time has passed.

You lose money when you buy – hand over fist over foot over wallet, you lose money when you buy.

You make money in property investing when you H O L D.

ENTRY COST

To buy a property you not only need a deposit, but you also need to pay stamp duty, building and pest inspections or maybe a strata report. Legal fees too. Then there’s all the time you spent researching, arranging finance, visiting open inspections, haggling, signing contracts.

There’s a colossal expense involved in buying a property. There is no way you can buy a property in Australia and make money when you buy.

The people who make money when you buy are real estate agents, property developers, sellers, conveyancers and so on.

YOU MAKE MONEY HOLDING

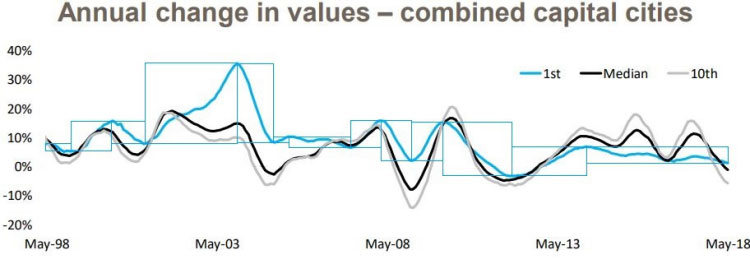

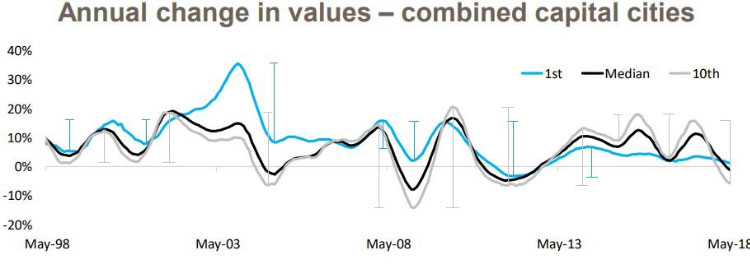

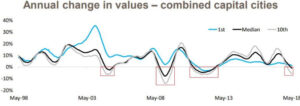

You make back all that money if you hold and let capital growth do its thing. If you’ve bought in a bad location, it can take many years for it to recover lost ground. But even if you’ve bought in a belter, you still have to wait at least 6 months to recoup the costs associated with entering the market.

WHO SAYS THIS?

I know what you’re thinking. I’m taking the expression too literally. What it really means Jeremy, is that if you buy a property for a good price, you’ve locked in some immediate equity at the time you buy.

But again, this is not only wrong, but bad advice.

This advice makes an investor focus too much on buying under market value, chasing a good deal, getting a bargain. The easiest suburbs to buy under market value are the ones that are experiencing negative growth, that is, the very worst investment markets.

“The best investment markets are the ones where buying under market value is virtually impossible”

Don’t focus on buying cheaply – you haven’t made a profit. What you’ve probably done is bought in a dud location.

For more on this, check out another presentation in this series titled:

IRRELEVANT

Whatever saving you think you’re going to make buying cheaply will be comfortably and quickly overwhelmed by the movement in the market over the next 6 to 12 months. If you’ve bought in a market that hasn’t moved in that period, then you’ve just incurred an opportunity cost. And that opportunity cost will be so much more than the paltry gain you think you made buying cheaply.

“I would much rather pay over market value for a property in a hot market than pay under market value for a property in a flat or falling market”

STRATEGY

If your property investment strategy is based on achieving good capital growth, then every month after you’ve bought, is another month you’re moving forwards. If, however, the key to your investment success hangs on buying well, how can you do that every month?

CONCLUSION

Your focus as an investor should be on making money as you hold, not when you buy. Be aware of the high costs to enter the market and you’ll put a lot more effort into researching the right locations. Your research should be focussed on what is going to happen after you’ve bought. Don’t focus on buying well, focus on finding properties that will grow well as you hold onto them.

I’ve got a couple of other presentations on similar topics you might be interested in. Check these out:

“No advantage buying under median value”

“Aiming to buy under market value is bad”

That 2nd one in particular is a beauty. It shows there’s no such thing as the discount-flip strategy. You don’t make money when you buy.

Tagged:

Ep. 34: Nobody Told Me… The Realities of Property Investing

In this episode, we get real about the industry’s biggest red flags—misleading claims, flashy marketing tactics, and so-called “experts” who might not have your best interests at heart. From high-pressure sales tactics to the long-term excuse for bad investments,...

Ep. 33: How to Protect Yourself from Oversupply

Oversupply is one of the biggest risks in property investing 🏡 In this episode, we break down how to spot areas at risk of too much stock and what to look for before buying. We’ll show you why counting listings isn’t enough, how to use Google Maps to predict future...